· The Cashback Real Estate Team · Home Buying · 9 min read

The Home Buying Process: A Step-by-Step Guide for First-Time Buyers

Buying a home is one of the biggest financial decisions you'll ever make. Understanding each step of the process — from getting pre-approved to picking up the keys — takes the mystery out of it and puts you firmly in control.

Buying a home for the first time can feel like learning a new language. Escrow. Pre-approval. Earnest money. Title insurance. The terminology alone is enough to make your head spin. But when you break the journey down into clear, manageable steps, what once seemed overwhelming becomes an exciting — and achievable — milestone.

This guide walks you through every stage of the home buying process, from your very first financial check-up to the moment you turn the key in your own front door.

Step 1: Assess Your Financial Health

Before you look at a single listing, spend time getting an honest picture of where you stand financially. This means reviewing your credit score, calculating your debt-to-income ratio, and figuring out how much you have saved for a down payment.

Your credit score is one of the most important factors lenders use when deciding your mortgage rate. A score above 740 typically qualifies you for the best rates available. If your score needs work, focus on paying down credit card balances, disputing any errors on your report, and avoiding new credit inquiries for at least six months before applying.

Your debt-to-income ratio (DTI) is the percentage of your gross monthly income that goes toward debt payments. Most conventional lenders prefer a DTI below 43%, and the lower the better. If your DTI is high, paying off an installment loan or reducing revolving debt before applying can meaningfully improve your buying power.

As for the down payment: while 20% is the gold standard that lets you avoid private mortgage insurance (PMI), many loan programs accept as little as 3% to 3.5% down. Just be aware that a smaller down payment means higher monthly costs and more interest paid over the life of the loan.

Step 2: Get Pre-Approved for a Mortgage

Pre-approval is not the same as pre-qualification. Pre-qualification is a rough estimate based on numbers you self-report. Pre-approval involves a lender actually pulling your credit, verifying your income and assets, and issuing a conditional commitment to lend you a specific amount at a specific rate.

Sellers take pre-approved buyers far more seriously. In a competitive market, submitting an offer without a pre-approval letter is almost like showing up without ID — you simply won’t be taken seriously.

To get pre-approved, you’ll typically need to provide:

- Two years of W-2s or tax returns (self-employed buyers may need more)

- Recent pay stubs (usually the last 30 days)

- Two to three months of bank statements

- Photo ID

- A signed authorization for a credit check

Shop at least two or three lenders before committing. Rates, fees, and service levels can vary significantly, and a small difference in your interest rate compounds into thousands of dollars over a 30-year loan.

Step 3: Define What You’re Looking For

With a pre-approval in hand, you now know your budget. The next step is deciding what to do with it. This means getting specific about your needs versus your wants.

Needs are non-negotiables: the number of bedrooms required for your household, a ground-floor bedroom if mobility is a concern, proximity to your workplace, or access to a specific school district.

Wants are features you’d love to have but could live without: a home office, a larger backyard, an open-plan kitchen, or a two-car garage.

Be honest with yourself about which is which. In most markets you won’t find a home that checks every box, so knowing your hierarchy of priorities in advance prevents you from either compromising on what truly matters or passing on a great property over something trivial.

Also think about neighborhood, not just the house. The school district, walkability, local crime statistics, future development plans, and the commute time to work all significantly affect both your quality of life and the home’s long-term value.

Step 4: Find a Buyer’s Agent

A buyer’s agent works exclusively for you — not the seller — and their job is to help you find the right property, make a competitive offer, negotiate on your behalf, and navigate the transaction through to closing. In most transactions, the seller pays the buyer’s agent’s commission, which means you typically receive their expertise at no direct cost to you.

If you work with a cashback realtor, you can go a step further. A cashback agent rebates a portion of their commission back to you at closing, potentially putting thousands of dollars in your pocket. On a $400,000 purchase, a 1% rebate is $4,000 — enough to cover closing costs, fund immediate repairs, or replenish savings after your down payment.

When choosing an agent, look for someone with strong local market knowledge, a track record of successful transactions in your price range, and clear communication. You’ll be working closely with this person under pressure, so trust and responsiveness matter as much as credentials.

Step 5: Search for Homes

Now the part most people picture when they imagine buying a house: the search. Your agent will set up an MLS feed filtered to your criteria so you’re notified as soon as matching properties hit the market. In a fast-moving market, acting quickly matters — desirable homes can receive multiple offers within days of listing.

Visit properties in person whenever possible, even homes that don’t look perfect in photos. Photographs can both flatter and mislead. A home that photographs awkwardly may feel wonderful when you walk through it; a beautifully staged photo spread can mask real problems.

Keep notes on every home you visit. After a week of showings, they start to blur together, and having specific observations about each property — what you loved, what concerned you, what questions came up — makes it far easier to compare and decide.

Step 6: Make an Offer

When you find the right home, your agent will help you craft a competitive offer. The offer price is just one element. Other terms that matter include:

- Earnest money deposit — Typically 1–3% of the purchase price, submitted with the offer to demonstrate you’re a serious buyer. It goes toward your down payment at closing but can be forfeited if you back out without a valid contingency.

- Contingencies — Clauses that let you exit the contract without penalty under certain conditions. The most important are the inspection contingency (which protects you if the home inspection reveals serious problems) and the financing contingency (which protects you if your mortgage falls through).

- Closing date — Sellers often have strong preferences here. Offering flexibility on timing can make your bid more attractive even if it isn’t the highest offer.

- Personal property — Confirm which appliances, fixtures, and items are included in the sale.

Your agent will advise on pricing strategy based on recent comparable sales (known as “comps”) in the neighborhood. Bidding too low risks insulting the seller or losing the home; bidding too high risks overpaying. Getting this calibration right is where an experienced agent earns their place.

Step 7: Negotiate and Go Under Contract

The seller will accept your offer, reject it, or counter it. Negotiation often goes several rounds. Your agent manages this process and helps you evaluate whether proposed changes are reasonable.

Once both parties agree on all terms, you sign the purchase agreement and the home officially goes “under contract.” The clock now starts ticking on your contingency deadlines.

Step 8: Complete Due Diligence

The period between going under contract and closing is when you do your homework. This typically includes:

Home Inspection — Hire a licensed inspector to evaluate the physical condition of the property: structure, roof, electrical systems, plumbing, HVAC, and more. The inspector’s job is to be your eyes and ears. Their report may identify issues ranging from minor maintenance items to serious structural problems. Depending on what’s found, you can request repairs, ask for a price reduction, or — if the issues are severe enough — walk away.

Appraisal — Your lender will order an independent appraisal to confirm the home is worth what you’re paying. If the appraisal comes in below the purchase price, you’ll need to renegotiate with the seller, make up the difference in cash, or exit the contract using your financing contingency.

Title Search — A title company will research the property’s ownership history to ensure the seller has clear legal title to convey and that there are no outstanding liens, unpaid taxes, or legal disputes attached to the property.

Final Walkthrough — Conducted typically 24–48 hours before closing, this is your last chance to confirm the home is in the agreed condition, that any negotiated repairs have been completed, and that no new damage has occurred since your inspection.

Step 9: Close on Your Home

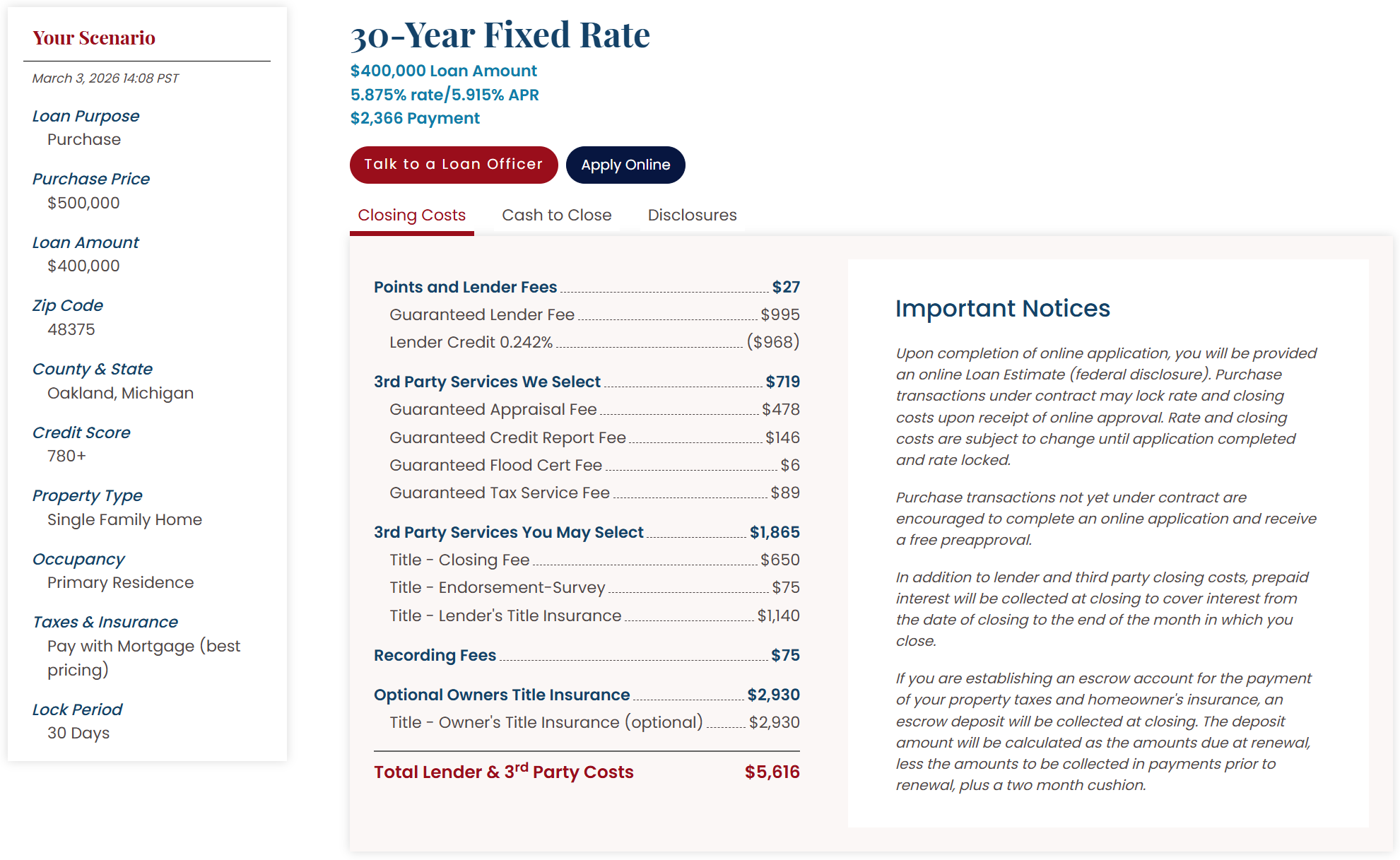

Closing is the legal transfer of property ownership. You’ll sign a significant stack of documents, pay your closing costs and any remaining down payment, and receive the keys.

Closing costs typically range from 2% to 5% of the loan amount and include lender fees, title insurance, prepaid property taxes and homeowner’s insurance, and escrow fees. Review your Closing Disclosure carefully before settlement day — it details every charge and should closely match the Loan Estimate you received earlier in the process.

If you’re working with a cashback realtor, your rebate will typically appear as a credit on the closing disclosure, directly reducing what you owe at the table.

You’re a Homeowner

Buying a home is a process with many moving parts, but none of them are beyond your understanding or control. The buyers who navigate it most successfully are those who come prepared — financially, informationally, and emotionally. They know their numbers, they find the right support, and they take each step deliberately rather than reactively.

If you’re ready to begin, the first step is simpler than it seems: check your credit score, call a lender, and start the conversation. Everything else follows from there.

Ready to work with an agent who puts money back in your pocket? Ask about our cashback program — real buyers have received thousands of dollars back at closing without sacrificing an ounce of service.