· Home Buying · 6 min read

Understanding Your Mortgage Quote — A Michigan Homebuyer's Guide

Learn how to read a real mortgage quote, shop rates after your offer is accepted, and know exactly how much cash you'll need to bring to the closing table.

You found a home you love in Oakland County. Your offer was accepted. Now a page full of numbers is staring back at you — interest rates, APRs, lender credits, title fees, escrow deposits. What does it all mean, and what do you actually need to do next?

This post walks through a real mortgage quote (a 30-year fixed rate loan on a $500,000 purchase in zip code 48375) and explains every piece — including the one thing most buyers don’t know: you are not locked into the bank that gave you your pre-approval letter.

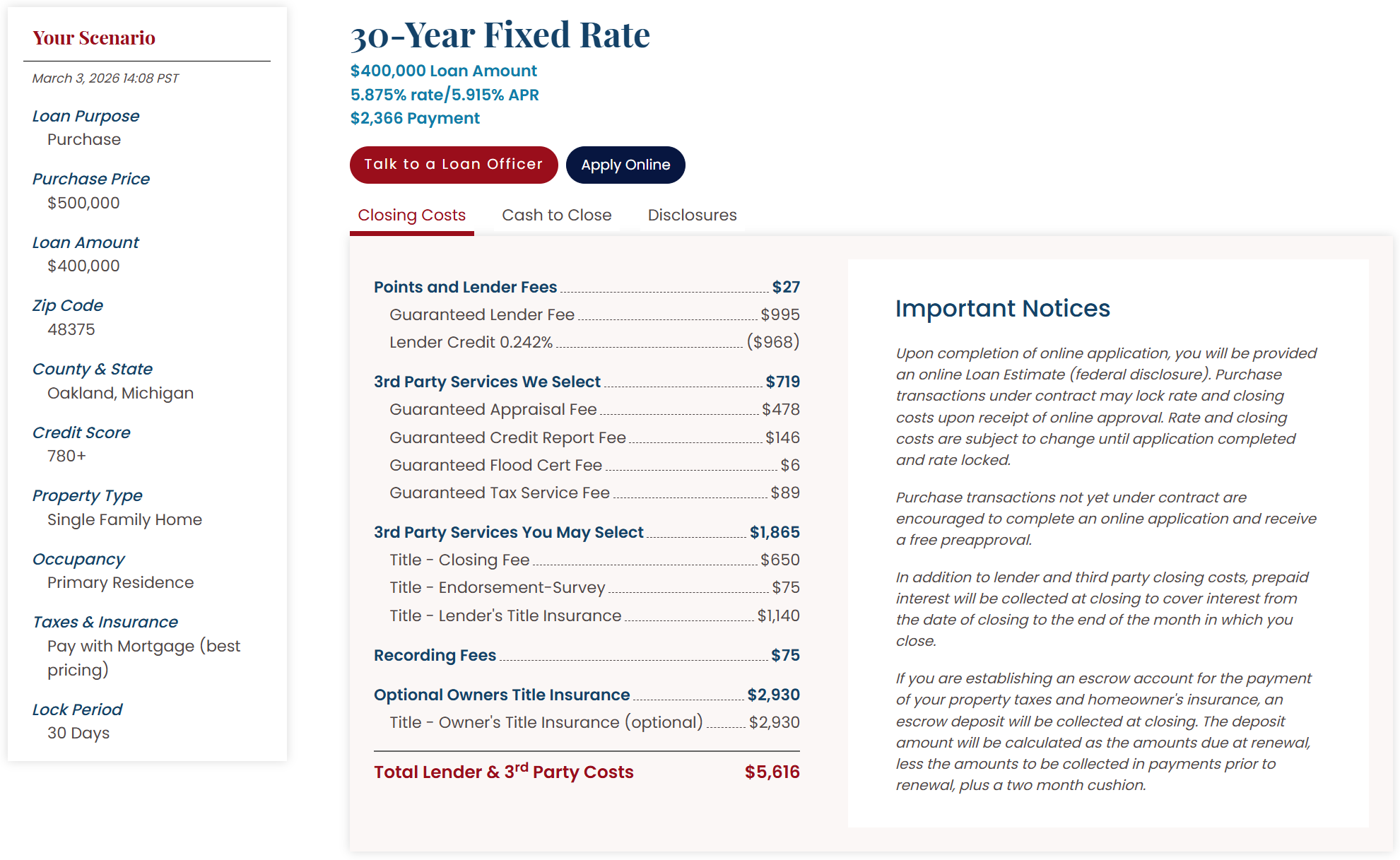

How to Read a Mortgage Quote

The quote in our example shows the following key terms:

- Loan Amount: $400,000 (80% of the $500,000 purchase price — the buyer puts 20% down)

- Rate: 5.875%

- APR: 5.915%

- Monthly Payment: $2,366

Rate vs. APR — What’s the Difference?

The interest rate (5.875%) is what the lender charges you to borrow. The APR (Annual Percentage Rate, 5.915%) is slightly higher because it folds in certain lender fees spread across the life of the loan. When comparing offers from multiple lenders, use the APR — it’s the more honest apples-to-apples number.

What the Monthly Payment Doesn’t Include

The $2,366 payment covers principal and interest only. It does not include:

- Property taxes (estimated separately, paid through escrow)

- Homeowner’s insurance (also collected in escrow)

For a $500,000 home in Oakland County, budget roughly $500–$700/month on top of P&I for taxes and insurance. Your real all-in monthly housing cost is closer to $2,900–$3,100.

How to Get an Online Quote

Sites like AIMloan.com, Bankrate, and LenderFi let you enter your scenario — purchase price, down payment, zip code, credit score, property type, lock period — and return real rate quotes in seconds, often without a hard credit pull.

This is exactly what the screenshot shows: a quote generated for a 780+ credit score buyer purchasing a single-family primary residence with a 30-day rate lock in zip code 48375.

When shopping online quotes, always use identical inputs across every lender. Even a small difference — changing the lock period from 30 to 45 days, or toggling taxes from “pay separately” to “pay with mortgage” — will shift the numbers and make comparisons meaningless.

What to compare across quotes:

- Interest rate and APR

- Points and Lender Fees (net, after any lender credits)

- Which third-party costs are marked “guaranteed” vs. estimates

- Lock period length

Shopping Rates After Your Offer Is Accepted

You do not have to use the lender who gave you your pre-approval letter.

This is one of the most overlooked facts in home buying. Your pre-approval letter served one purpose: it proved to the seller that a real lender has reviewed your finances and is willing to fund the deal. That got your offer accepted. Its job is done.

The moment the seller signs the purchase agreement, you are free to shop any lender you want for your actual mortgage.

Why It Matters

A 0.25% difference in rate on a $400,000 loan is roughly $60/month — more than $21,000 over 30 years. Even a 0.125% difference saves over $10,000. That’s real money, and it costs nothing to collect a few extra quotes.

How to Do It

After your offer is accepted, you typically have 30–45 days until closing. Use the first 7–10 days to apply with 3–5 lenders. Under federal law (RESPA), every lender must provide a standardized Loan Estimate within 3 business days of your application. This makes side-by-side comparison straightforward.

Once you’ve chosen the best offer, lock your rate in writing. Then notify your real estate agent which lender you’re proceeding with.

One important note: choose a lender with a strong reputation for closing on time. A lender who misses the closing date can cost you the deal and your earnest money deposit. Cheap but slow is worse than slightly more expensive and reliable.

Understanding Closing Costs

The quote breaks closing costs into four buckets. Here’s what each one means:

1. Points and Lender Fees — $27 (net)

This line looks nearly free, but there’s more going on underneath:

| Item | Amount |

|---|---|

| Guaranteed Lender Fee | $995 |

| Lender Credit (0.242%) | ($968) |

| Net | $27 |

A lender credit means the lender slightly raises your interest rate in exchange for cash toward your closing costs. It is not free money — you pay for it over time through a higher rate. In this case, the credit nearly wipes out the origination fee, resulting in a net cost of just $27.

2. 3rd Party Services the Lender Selects — $719

These are required services where the lender chooses the provider. You generally cannot shop for alternatives.

| Item | Amount |

|---|---|

| Appraisal Fee | $478 |

| Credit Report Fee | $146 |

| Flood Certification Fee | $6 |

| Tax Service Fee | $89 |

3. 3rd Party Services You May Select — $1,865

Title-related fees fall here — and you can shop these. Call 2–3 title companies in your area and compare. Savings of $200–$400 are common.

| Item | Amount |

|---|---|

| Title – Closing Fee | $650 |

| Title – Endorsement-Survey | $75 |

| Title – Lender’s Title Insurance | $1,140 |

4. Recording Fees — $75

County government fees to record the deed and mortgage in public records. Fixed and non-negotiable.

Optional: Owner’s Title Insurance — $2,930

This is listed separately because it is optional — but it protects you, not the lender. The lender’s title insurance (above) only protects the bank if a title problem surfaces. Owner’s title insurance protects your equity if an old lien, forged document, or unknown heir surfaces after closing.

It is a one-time premium paid at closing, and for older properties especially, it is strongly recommended.

Total Lender & 3rd Party Costs: $5,616

Cash to Close

Cash to close is the total amount you wire to the closing table. It is significantly more than your down payment alone.

For this scenario, expect approximately:

| Item | Estimated Amount |

|---|---|

| Down Payment (20%) | $100,000 |

| Lender & 3rd Party Closing Costs | $5,616 |

| Prepaid Interest (closing date → end of month) | ~$400–$700 |

| Escrow Deposit (taxes + insurance cushion) | ~$3,000–$6,000 |

| Estimated Total | ~$109,000–$112,000 |

Your lender will send a Closing Disclosure at least 3 business days before your closing date with the exact final number.

⚠️ Wire Fraud Warning: Never wire closing funds based on email instructions alone. Before sending any wire, call your title company directly at a phone number you obtained independently — not one from the email — to verify routing and account numbers. Wire fraud targeting homebuyers is common and the transfers are typically unrecoverable.

Summary: Your Action Checklist

- Get your pre-approval — shop 1–2 lenders, use the best letter to submit your offer

- Get your offer accepted — the pre-approval letter’s job is now done

- Shop rates immediately — apply with 3–5 lenders in the first week, compare Loan Estimates

- Lock your rate with the best combination of rate, fees, and lender reliability

- Review your Closing Disclosure 3 days before closing — verify every number

- Wire funds safely — confirm routing numbers by phone, never by email

The mortgage process has more moving parts than most buyers expect, but once you understand what each line means, you’re no longer at the mercy of a single lender’s quote. A little comparison shopping after your offer is accepted can save you tens of thousands of dollars over the life of your loan.

Rates shown are for illustrative purposes based on a sample quote dated March 3, 2026. Rates change daily. Always obtain a current Loan Estimate from a licensed lender. This post is for educational purposes only and does not constitute financial or legal advice.